ESG history

Description de l'article de blog :

4/19/20257 min čitanje

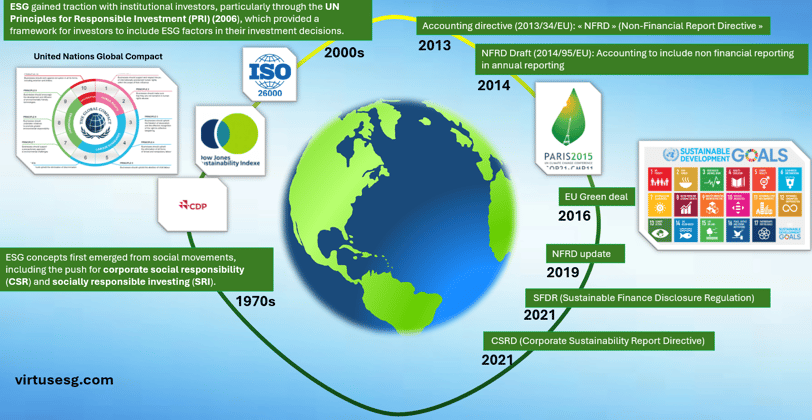

The evolution of Environmental, Social, and Governance (ESG) and Corporate Social Responsibility (CSR) concepts has been significantly shaped by a series of legislative milestones. Beginning with the Paris Agreement, which set the stage for global climate action, the discourse expanded with directives such as the Non-Financial Reporting Directive (NFRD) and the Pacte Law, which emphasize the accountability of corporations in reporting their sustainability practices. The Sustainable Finance Disclosure Regulation (SFDR) further strengthens this movement by enhancing transparency in financial markets regarding sustainability. Most recently, the Corporate Sustainability Reporting Directive (CSRD) aims to standardize reporting requirements across the EU, ensuring that companies contribute to broader sustainable development goals. These developments underscore an increasing acknowledgment of sustainability's crucial role in the corporate and regulatory landscape, reflecting a collective effort to align business practices with global sustainability objectives.

I. Historical Overview of ESG and Related Concepts

1. The Emergence of ESG (Environmental, Social, and Governance)

Early 2000s: The concept of ESG began to take shape, with a milestone in 2004 when the term gained prominence through a report titled “Who Cares Wins”. This report resulted from an initiative led by Kofi Annan, then UN Secretary-General, who convened more than 50 CEOs of major global financial institutions to discuss sustainable development.

Objective: To integrate environmental, social, and governance (ESG) considerations into financial markets and investment decisions.

Key Recommendation: The report urged that ESG factors be incorporated into financial analysis and investment strategies, advocating for long-term sustainable investments that benefit both society and investors.

Turning Point: This initiative marked a significant shift, prompting the growth of responsible investment practices and encouraging the integration of ESG factors into investment decisions.

2006: The UN-supported Principles for Responsible Investment (PRI) were launched, establishing a framework for incorporating ESG into investment practices. The PRI quickly gained global recognition and became a standard for responsible investment.

Growth and Influence: Since then, ESG’s importance in investment decisions has only grown, influencing corporate operations and how companies are evaluated by investors, regulators, and the public. ESG is now essential in assessing both risks and opportunities, reflecting a broader understanding of corporate value beyond mere financial performance.

2. Socially Responsible Investment (SRI)

Origins: The concept of Socially Responsible Investment (SRI) began to emerge as early as the 1920s, but it gained momentum during the 1960s and 1970s. Investors began to seek ways to align their portfolios with their ethical values, focusing on excluding companies involved in controversial activities such as arms sales or tobacco production.

Modern SRI: Today, specialized investment funds, often called “Ethical Funds,” focus exclusively on investing in companies that adhere to ESG and Corporate Social Responsibility (CSR) standards. These funds typically avoid securities from companies that do not meet these criteria.

3. Corporate Social Responsibility (CSR)

Definition: Corporate Social Responsibility (CSR) refers to a business’s obligation to integrate social, environmental, and governance concerns into their strategies. The term’s equivalent in English is CSR (Corporate Social Responsibility).

Historical Evolution:

Early 20th Century: The roots of CSR can be traced back to the concept of benevolent capitalism, where industrial philanthropists believed business owners had moral responsibilities toward their employees and society.

1950s and 1960s: CSR became more structured, particularly in the United States, with scholars such as Howard Bowen (often called the “father of CSR”) developing the idea that businesses had responsibilities beyond profit generation. His book, “Social Responsibilities of the Businessman” (1953), emphasized the ethical responsibilities of corporations.

1970s and 1980s: CSR gained further importance, with growing concerns about environmental protection, human rights, fair labor practices, and consumer rights. Disasters like the Bhopal chemical leak (1984) sparked awareness in the West of the need for corporate accountability.

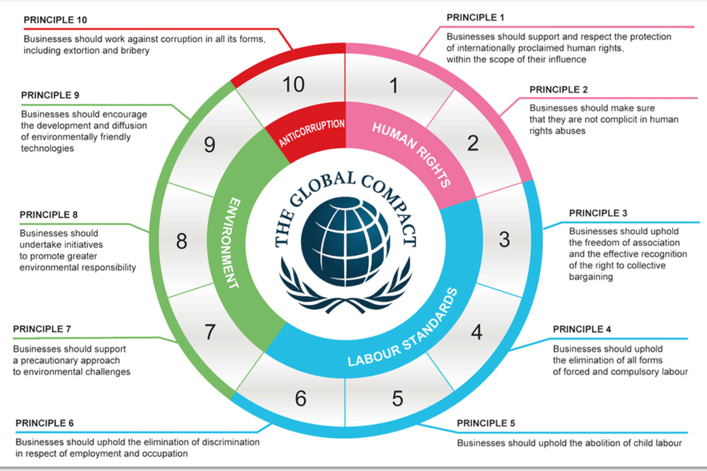

1990s and 2000s: Globalization and corporate scandals heightened the need for companies to adopt responsible business practices. International organizations like the United Nations promoted CSR through initiatives such as the UN Global Compact in 2000. Companies began incorporating CSR into their core strategies, guided by standards such as the OECD Guidelines for Multinational Enterprises and the ISO 26000 social responsibility standard.

2010s to Present: CSR is now an integral part of corporate management, with special attention to the UN Sustainable Development Goals (SDGs) and the growing importance of ESG criteria in investment decisions. Companies are increasingly required to report on their social and environmental impacts, with CSR viewed as a means to ensure long-term sustainability.

4. The Concept of Sustainable Development

Popularization: The modern concept of sustainable development was brought to global attention by the 1987 Brundtland Report ("Our Common Future"), which called on economic and institutional stakeholders to address the environmental and social impacts of their activities.

Key Milestones:

1992 Earth Summit in Rio: This United Nations conference highlighted the importance of integrating environmental considerations into economic development.

1999: The launch of the Dow Jones Sustainability Index provided a key tool for evaluating companies' performance on sustainability. It was followed by the creation of the Carbon Disclosure Project (CDP) in 2000, encouraging companies to disclose their greenhouse gas emissions and climate change strategies.

Link to ESG: While the ESG framework was formally developed in the early 2000s, its foundations are rooted in long-standing efforts to address ethical, social, and environmental concerns in business and investment decisions. Sustainable development remains a key element of ESG strategies today.

II. The Legal Framework

a) The Paris Agreement

The Paris Agreement is an international treaty adopted on December 12, 2015, which entered into force on November 4, 2016. It has now been ratified by 196 parties, including the European Union and the United States.

Objective: Its main goal is to limit global warming to 1.5 to 2 degrees Celsius and to achieve a climate-neutral world by the mid-21st century.

Follow-up Legislation: National, European, and international laws enacted after the Paris Agreement translate this overarching objective into binding legal measures.

b) The Non-Financial Reporting Directive (NFRD) and DPEF

The Declaration of Non-Financial Performance (DPEF) was introduced by Directive 2013/34/EU, also known as the Non-Financial Reporting Directive (NFRD).

2019 Update: The NFRD was updated in 2019 to include the principle of double materiality and align with the Paris Agreement objectives.

Double Materiality: Under this principle, companies must provide a report on both financial and non-financial impacts, focusing on elements that may affect the company’s current and future financial health.

Impact Report: Initially, the impact report was meant to explain how governance factors influenced the company's future. However, this aim was not fully achieved, leading to stricter reporting requirements in subsequent years.

c) Sustainable Finance Disclosure Regulation (SFDR)

The Sustainable Finance Disclosure Regulation (SFDR) aims to harmonize and increase transparency around ESG (Environmental, Social, and Governance) criteria in the financial sector.

Enactment: The SFDR came into effect on March 10, 2021 and applies directly across all EU member states, including France.

Requirements: Financial institutions must disclose how they integrate ESG risks and opportunities into their investment decisions and advice. This includes publishing information on sustainability policies and the impact of investments on ESG factors.

Global Reach: While the SFDR applies within the EU, it also affects non-EU companies seeking to attract EU investors. These companies must meet SFDR transparency standards when marketing financial products in the European market.

d) Corporate Sustainability Reporting Directive (CSRD)

In April 2021, the European Commission proposed the Corporate Sustainability Reporting Directive (CSRD) to strengthen the standards set by the NFRD.

Adoption and Enforcement: The directive was formally adopted on November 10, 2022, and will apply in the EU from November 2024, unless transposed earlier by member states. In France, the directive has been in effect since January 2024.

Objective: The CSRD aims to measure the environmental, social, and ecosystem impacts of companies and to ensure that reports are standardized and comparable across businesses.

Addressing Greenwashing: The CSRD responds to the weaknesses of the NFRD, where some companies used vague or unverifiable metrics in reports, often engaging in greenwashing. The new directive introduces standardized and mandatory reporting norms, with a focus on carbon accounting and sustainability.

Global Coordination: The CSRD aligns with global initiatives on carbon accounting but highlights some ongoing differences, notably between the EU and the US, regarding how to account for and present companies' carbon footprints.

e) Corporate Sustainability Due Diligence Directive (CSDD)

The proposed Corporate Sustainability Due Diligence Directive (CSDD), influenced by French legislation, is currently being discussed in the European Parliament.

Focus: The CSDD specifically targets ESG due diligence requirements, distinct from the anti-corruption and anti-fraud obligations introduced by the Sapin II Law.

Due Diligence Requirements: Companies must identify and mitigate negative impacts on human rights and the environment in their supply chains. This directive focuses on large companies with complex global value chains and aims to integrate sustainability into corporate governance.

Green Economy: The CSDD encourages companies to contribute to a green, carbon-neutral economy in line with the European Green Deal and the UN Sustainable Development Goals (SDGs).

Complementarity: The CSDD complements other EU initiatives like the CSRD and SFDR, helping to create a cohesive framework that encourages companies to operate more responsibly and sustainably.

Conclusion

This overview highlights the evolution of sustainability regulations, from the early notions of corporate social responsibility to the adoption of the Corporate Sustainability Reporting Directive (CSRD) by the European Union.

By emphasizing the growing importance of ESG principles in corporate governance and regulatory frameworks, this summary illustrates the shift towards a more sustainable and responsible economy.

For more information on the application of the CSRD, please refer to our dedicated article on CSRD and the new corporate obligations.

Virtus ESG

Tailored compliance solutions for your business needs.

Company

KONTAKT

contact(@)virtusesg.com

+385 99 6984 953

© 2025. All rights reserved.

BOULEUMA j.d.o.o.

MBS: 110150987

MB: 6098126

OIB: 51010117689

VAT: HR51010117689

Šibenik, Hrvatska